Overview of Retire Young Retire Rich Intl

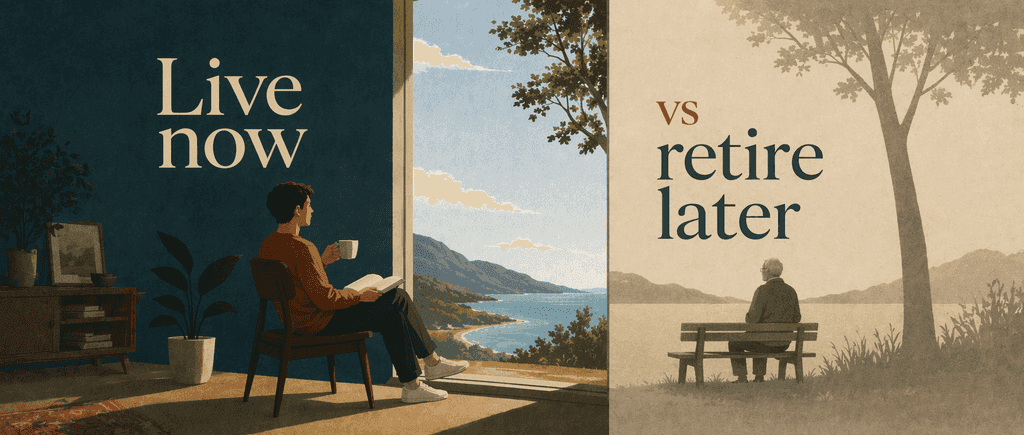

Kiyosaki's wealth manifesto challenges conventional retirement wisdom. Endorsed by Oprah and selling 32+ million copies across 51 languages, this counterintuitive guide asks: Why work until 65 when financial freedom could be yours decades earlier? The rich don't save - they leverage.

- Leverage debt strategically to acquire income-generating assets instead of liabilities.

- Financial literacy is your greatest asset for long-term wealth creation and protection.

- Pay yourself first by automating savings before covering expenses or bills.

- Build your asset column with cash-flowing investments before focusing on income growth.

- Replace “I can’t afford it” with “How can I afford it?” to unlock financial creativity.

- Develop habits that prioritize financial freedom over traditional job security.

- Use corporate structures and tax strategies to protect and grow wealth.

- Shift from earning paychecks to creating systems that generate passive income.

- Continuous learning in money management outperforms relying solely on formal education.

- Wealth is measured by how long you can sustain your lifestyle without working.

About the Author of Retire Young Retire Rich Intl

Robert T. Kiyosaki, bestselling author of Rich Dad’s Retire Young Retire Rich, is a pioneering voice in personal finance and wealth-building education.

Born in 1947 in Hawaii, Kiyosaki’s work focuses on financial literacy, entrepreneurship, and challenging conventional views on money—themes rooted in his contrasting upbringing with a fiscally conservative father (“Poor Dad”) and a friend’s entrepreneur father (“Rich Dad”).

A U.S. Marine Corps veteran and former Xerox salesman, he later founded the global Rich Dad Company, which promotes financial education through books, board games like CASHFLOW 101, and seminars. His landmark book Rich Dad Poor Dad (1997) has sold over 26 million copies worldwide and spawned a series including The Cashflow Quadrant and Why "A" Students Work for "C" Students.

Known for his contrarian advice on assets vs. liabilities, Kiyosaki’s teachings are widely cited in investing circles and have been integrated into financial curricula globally.

FAQs About Retire Young Retire Rich Intl

What is Rich Dad's Retire Young Retire Rich about?

Rich Dad's Retire Young Retire Rich by Robert T. Kiyosaki teaches strategies to achieve financial freedom through leveraging debt, assets, and mindset shifts. The book emphasizes using "cash flow" and "leverage" to build wealth rapidly, retire early, and sustain prosperity. Key lessons include converting earned income into passive income streams and prioritizing asset acquisition over traditional job security.

Who should read Rich Dad's Retire Young Retire Rich?

This book targets aspiring entrepreneurs, real estate investors, and individuals seeking early retirement. It’s ideal for those open to non-traditional wealth-building strategies, such as using debt to purchase income-generating assets. Readers skeptical of conventional retirement plans or interested in Kiyosaki’s Rich Dad philosophy will find actionable insights.

Is Rich Dad's Retire Young Retire Rich worth reading?

Yes, for readers seeking unconventional financial strategies. Kiyosaki challenges the “work until 65” mindset, offering frameworks to accelerate wealth through leverage and cash flow optimization. Critics argue it oversimplifies risk, but its emphasis on financial education and asset-building makes it valuable for those open to entrepreneurial thinking.

How does leverage work in Retire Young Retire Rich?

Kiyosaki defines leverage as using borrowed capital or strategic partnerships to amplify returns. Examples include taking loans to invest in rental properties or businesses that generate passive income. He argues leverage accelerates wealth growth when applied to cash-flowing assets, contrasting it with reckless debt for liabilities.

What is the cash flow quadrant in Retire Young Retire Rich?

The cash flow quadrant categorizes earners as Employees, Self-Employed, Business Owners, or Investors. Kiyosaki urges readers to shift from the left side (trading time for money) to the right (building systems/assets). Investors and business owners achieve financial freedom faster by focusing on income-generating assets.

What mindset shifts does Kiyosaki recommend?

Kiyosaki advocates replacing fear-based financial habits with proactive strategies:

- View debt as a tool for asset acquisition.

- Prioritize financial education over traditional schooling.

- Focus on cash flow, not just salary.

These shifts aim to break the “rat race” cycle and build long-term wealth.

How does Retire Young Retire Rich differ from Rich Dad Poor Dad?

While Rich Dad Poor Dad introduces financial literacy basics, Retire Young Retire Rich delves into advanced leverage tactics and early retirement planning. The latter emphasizes speed, using real-world examples of how Kiyosaki and his wife retired financially free in under a decade.

What criticisms exist about Retire Young Retire Rich?

Critics argue the book underestimates risks of leveraging debt and oversimplifies real estate investing. Some note Kiyosaki’s strategies require significant upfront capital or risk tolerance, making them less accessible to low-income readers. However, supporters praise its paradigm-shifting approach to wealth.

How does Kiyosaki define financial freedom?

Financial freedom means having sufficient passive income from assets (rental properties, businesses, stocks) to cover living expenses without active work. Kiyosaki stresses this isn’t about extreme wealth but sustaining a desired lifestyle through cash flow.

What role does financial education play in the book?

Kiyosaki calls financial education the “foundation of wealth,” arguing schools teach outdated money management. He advocates self-education through books, mentors, and real-world practice to master concepts like tax strategies, market cycles, and asset valuation.

How does Retire Young Retire Rich address fear and greed?

The book identifies fear and greed as emotional barriers to wealth. Kiyosaki advises reframing fear into calculated risk-taking and redirecting greed toward asset-building rather than consumerism. This balance helps readers make rational, long-term financial decisions.

What are actionable steps from Retire Young Retire Rich?

- Audit finances: Differentiate assets (generate income) from liabilities (drain money).

- Acquire cash-flowing assets: Start small with rental properties or dividend stocks.

- Reinvest profits: Compound growth by channeling income into new investments.

- Leverage strategically: Use low-interest debt to scale asset portfolios

Feel the book through the author's voice

Turn knowledge into engaging, example-rich insights

Capture key ideas in a flash for fast learning

Enjoy the book in a fun and engaging way

Characters in Retire Young Retire Rich Intl

- Robert KiyosakiAuthor and investor who retired in his 40s

- Kim KiyosakiRobert's wife and partner in financial freedom

- Rich DadKiyosaki's mentor who taught him about leverage

- The Wright brothersCase study on embracing failure to achieve success

Key Themes in Retire Young Retire Rich Intl

- financial leverage

- passive income streams

- strategic debt management

- tax code optimization

- wealth mindset shift

Quotes from Retire Young Retire Rich Intl

The main reason people struggle financially is because they have spent years in school but learned nothing about money.

The single most powerful asset we all have is our mind.

Financial intelligence is simply having more options.

Debt, often feared by the middle class, becomes a powerful ally when used strategically.

Fast words create fast plans.

Explore Your Way of Learning

Quick Summary Mode

Quick Summary Mode

Read or listen to Retire Young Retire Rich Intl Summary in 8 Minutes

Break down key ideas from Retire Young Retire Rich Intl into bite-sized takeaways to understand how innovative teams create, collaborate, and grow.

Fun Mode

Fun Mode

Retire Young Retire Rich Intl Lessons Told Through 19-Min Stories

Experience Retire Young Retire Rich Intl through vivid storytelling that turns innovation lessons into moments you'll remember and apply.

Personalize Mode

Personalize Mode

Experience Retire Young Retire Rich Intl in your own learning style

Ask anything, choose your learning style, and co-create insights that truly resonate with you.

From Columbia University alumni built in San Francisco

"Instead of endless scrolling, I just hit play on BeFreed. It saves me so much time."

"I never knew where to start with nonfiction—BeFreed’s book lists turned into podcasts gave me a clear path."

"Perfect balance between learning and entertainment. Finished ‘Thinking, Fast and Slow’ on my commute this week."

"Crazy how much I learned while walking the dog. BeFreed = small habits → big gains."

"Reading used to feel like a chore. Now it’s just part of my lifestyle."

"Feels effortless compared to reading. I’ve finished 6 books this month already."

"BeFreed turned my guilty doomscrolling into something that feels productive and inspiring."

"BeFreed turned my commute into learning time. 20-min podcasts are perfect for finishing books I never had time for."

"BeFreed replaced my podcast queue. Imagine Spotify for books — that’s it. 🙌"

"It is great for me to learn something from the book without reading it."

"The themed book list podcasts help me connect ideas across authors—like a guided audio journey."

"Makes me feel smarter every time before going to work"

From Columbia University alumni built in San Francisco

"Instead of endless scrolling, I just hit play on BeFreed. It saves me so much time."

"I never knew where to start with nonfiction—BeFreed’s book lists turned into podcasts gave me a clear path."

"Perfect balance between learning and entertainment. Finished ‘Thinking, Fast and Slow’ on my commute this week."

"Crazy how much I learned while walking the dog. BeFreed = small habits → big gains."

"Reading used to feel like a chore. Now it’s just part of my lifestyle."

"Feels effortless compared to reading. I’ve finished 6 books this month already."

"BeFreed turned my guilty doomscrolling into something that feels productive and inspiring."

"BeFreed turned my commute into learning time. 20-min podcasts are perfect for finishing books I never had time for."

"BeFreed replaced my podcast queue. Imagine Spotify for books — that’s it. 🙌"

"It is great for me to learn something from the book without reading it."

"The themed book list podcasts help me connect ideas across authors—like a guided audio journey."

"Makes me feel smarter every time before going to work"

"Instead of endless scrolling, I just hit play on BeFreed. It saves me so much time."

"I never knew where to start with nonfiction—BeFreed’s book lists turned into podcasts gave me a clear path."

"Perfect balance between learning and entertainment. Finished ‘Thinking, Fast and Slow’ on my commute this week."

"Crazy how much I learned while walking the dog. BeFreed = small habits → big gains."

"Reading used to feel like a chore. Now it’s just part of my lifestyle."

"Feels effortless compared to reading. I’ve finished 6 books this month already."

"BeFreed turned my guilty doomscrolling into something that feels productive and inspiring."

"BeFreed turned my commute into learning time. 20-min podcasts are perfect for finishing books I never had time for."

"BeFreed replaced my podcast queue. Imagine Spotify for books — that’s it. 🙌"

"It is great for me to learn something from the book without reading it."

"The themed book list podcasts help me connect ideas across authors—like a guided audio journey."

"Makes me feel smarter every time before going to work"

"Instead of endless scrolling, I just hit play on BeFreed. It saves me so much time."

"I never knew where to start with nonfiction—BeFreed’s book lists turned into podcasts gave me a clear path."

"Perfect balance between learning and entertainment. Finished ‘Thinking, Fast and Slow’ on my commute this week."

"Crazy how much I learned while walking the dog. BeFreed = small habits → big gains."

"Reading used to feel like a chore. Now it’s just part of my lifestyle."

"Feels effortless compared to reading. I’ve finished 6 books this month already."

"BeFreed turned my guilty doomscrolling into something that feels productive and inspiring."

"BeFreed turned my commute into learning time. 20-min podcasts are perfect for finishing books I never had time for."

"BeFreed replaced my podcast queue. Imagine Spotify for books — that’s it. 🙌"

"It is great for me to learn something from the book without reading it."

"The themed book list podcasts help me connect ideas across authors—like a guided audio journey."

"Makes me feel smarter every time before going to work"

Download Summary of Retire Young Retire Rich Intl

Get the Retire Young Retire Rich Intl summary as a free PDF or EPUB. Print it or read offline anytime.